Stock price prediction based on wavelet transform and L2-LSTM

-

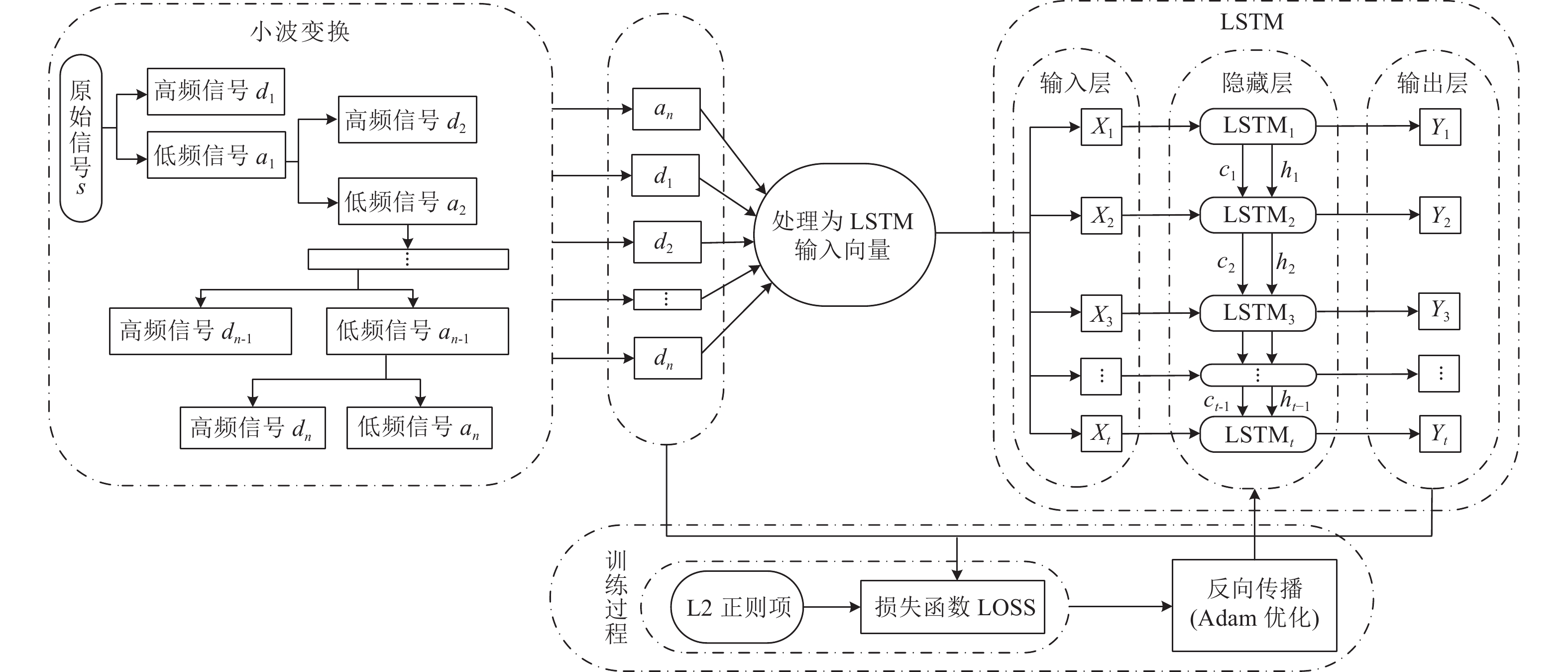

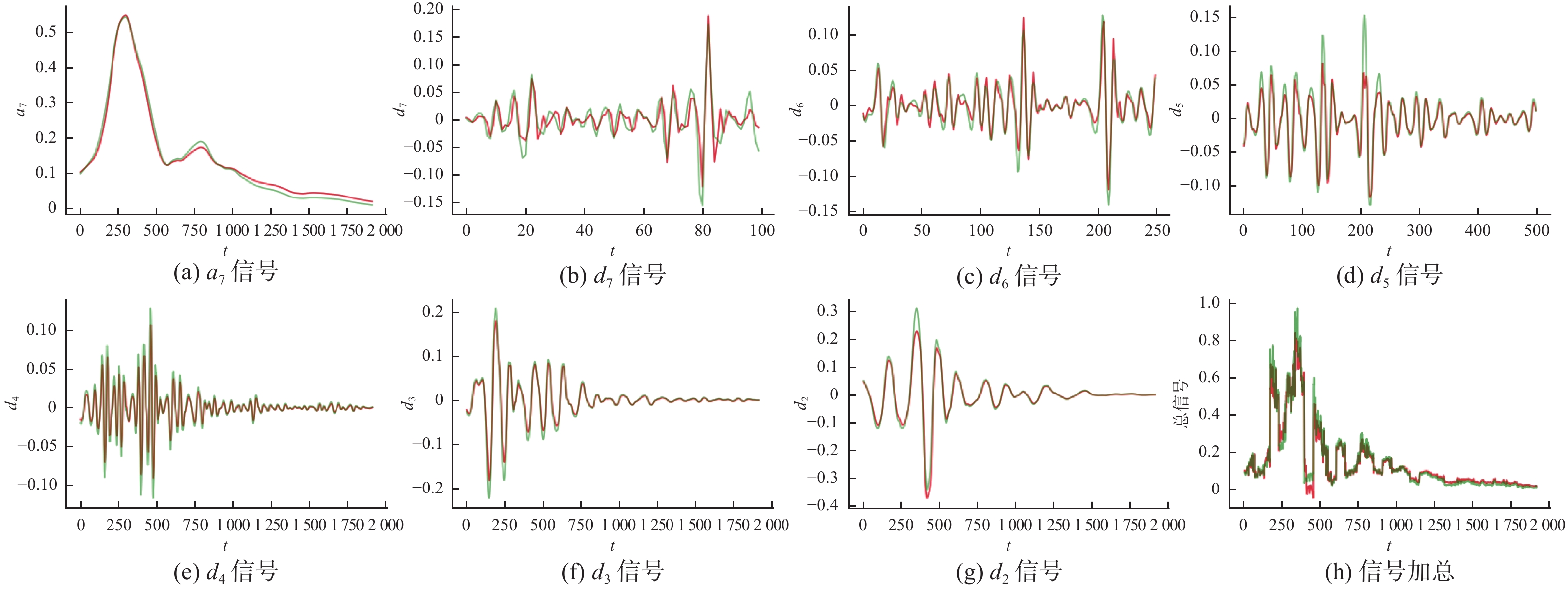

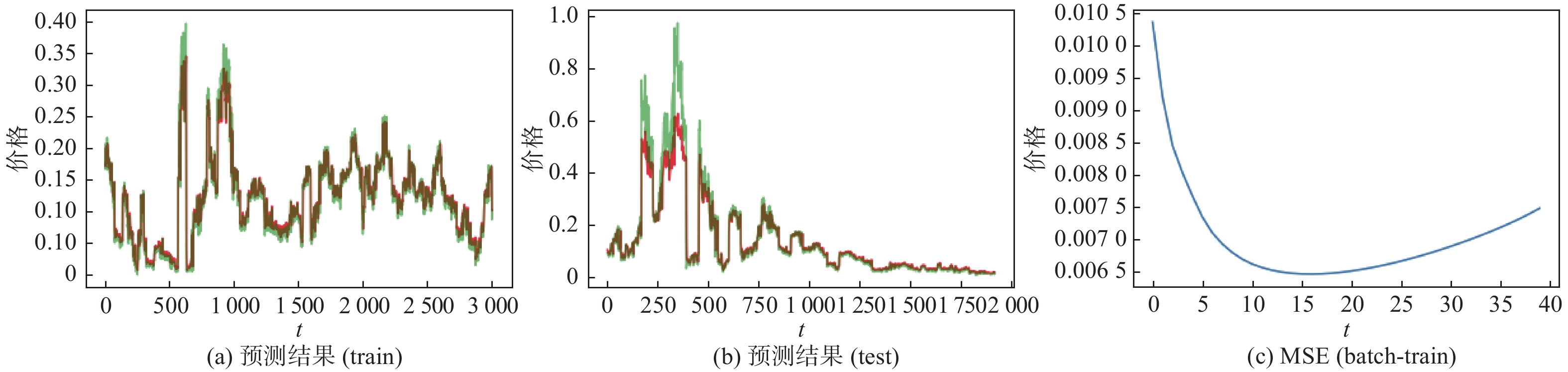

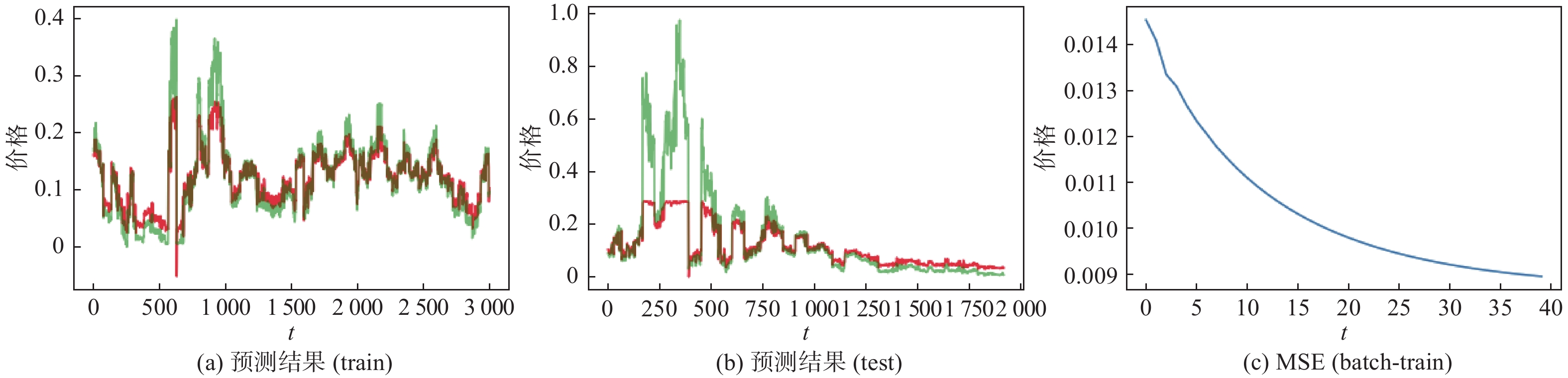

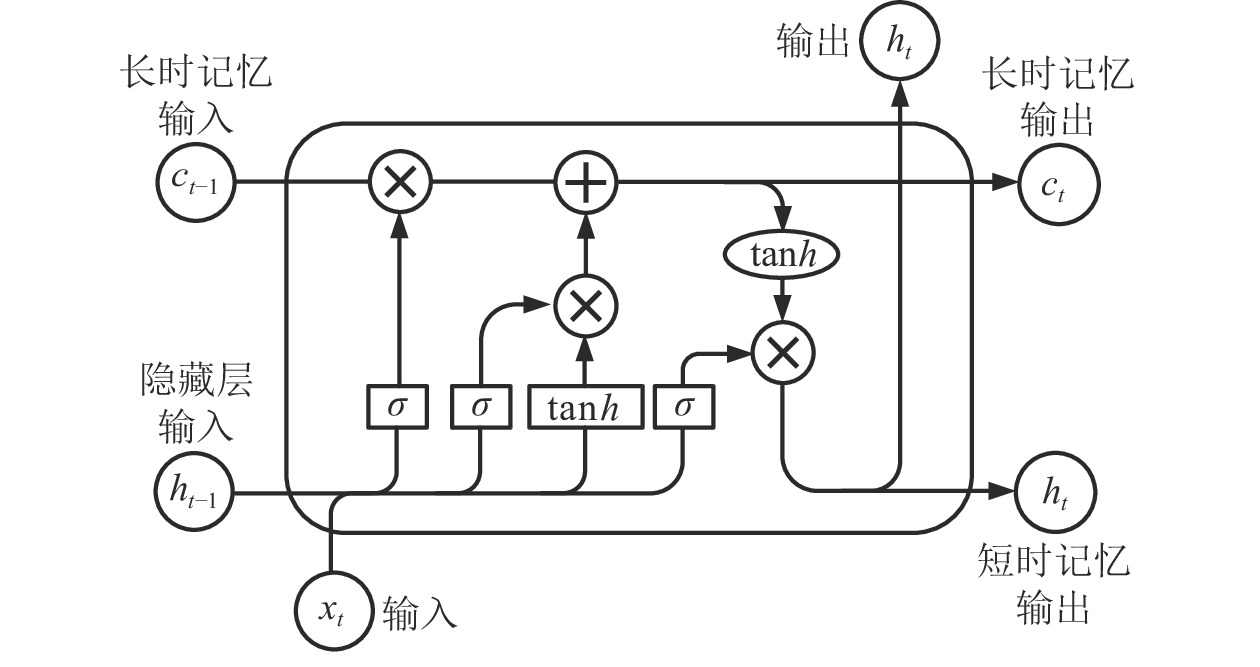

摘要: 长短时记忆网络(long short-term memory, LSTM)被广泛运用于股票的价格预测,但面对波动幅度较大的股票价格数据时,其预期效果不佳。提出一种基于小波变换和L2正则化LSTM的WT-L2-LSTM 模型,利用小波变换对原始宽频数据分解得到多层窄频数据,再逐层使用 L2正则化LSTM(L2-LSTM) 模型进行预测,分解后数据较平滑且可以逐层调参。预测结果显示,WT-L2-LSTM模型在拟合优度和均方误差上均优于LSTM模型,表明WT-L2-LSTM模型对股价预测具有更好的精度和泛化性能。Abstract: Long short-term memory (LSTM) networks are widely used for stock price prediction; however, their performance tends to be suboptimal when applied to stock price data with significant fluctuations. A novel WT-L2-LSTM model was proposed, which integrates wavelet transform with L2-LSTM. The original broadband data was decomposed into multiple layers of narrowband data using wavelet transform, and then the L2-LSTM model was used for the prediction layer by layer. The decomposed data is smoother and allows for parameter tuning layer by layer. The prediction results demonstrate that the WT-L2-LSTM model is superior to the LSTM model in terms of goodness of fit and mean square error, indicating that the WT-L2-LSTM model has better accuracy and generalization performance in predicting stock prices.

-

表 1 L2-LSTM模型评价指标

Table 1. Evaluation indicators of L2-LSTM model

评价指标 数值 评价指标 数值 MSE(train) 0.0007 MSE(test) 0.0131 MAE(train) 0.0172 MAE(test) 0.0529 r2(train) 0.7133 r2(test) − 1.2078 RMSE(train) 0.0259 RMSE(test) 0.1145  下载: 导出CSV

下载: 导出CSV

表 2 WT-L2-LSTM模型评价指标

Table 2. Evaluation indicators of WT-L2-LSTM model

评价指标 数值 评价指标 数值 MSE(train) 0.0003 MSE(test) 0.0031 MAE(train) 0.0104 MAE(test) 0.0241 r2(train) 0.9244 r2(test) 0.8283 RMSE(train) 0.0174 RMSE(test) 0.0559

下载: 导出CSV

表 3 3次实验结果对比(测试集)

Table 3. Comparison of three experiments results (test)

模型 MSE MAE r2 RMSE WT-L2-LSTM 0.0010 0.0192 0.9612 0.0319 L2-LSTM 0.0031 0.0241 0.8283 0.0559 LSTM 0.0131 0.0529 − 1.2078 0.1145

下载: 导出CSV

-

[1] 贺毅岳, 高妮, 韩进博, 等. 基于长短记忆网络的指数量化择时研究[J] . 统计与决策,2020,36(23):128 − 133. [2] 张妮. 基于LSTM 神经网络的股价预测应用研究[J] . 现代商业,2021(16):116 − 118. [3] 林勇. 基于深度学习和网络大数据的金融时间序列分析及预测[D] . 成都: 四川师范大学, 2022. [4] 周章元, 何小灵. 基于优化 LSTM 模型的股价预测方法[J] . 统计与决策,2023,39(6):143 − 148. [5] 欧阳玉龙. 基于金融时间序列与深度神经网络的股票市场预测性研究[D] . 南昌: 江西财经大学, 2021. [6] 乔泽东. 基于 WA-LSTM 的股指期货价格预测与择时策略研究[D] . 西安: 西北大学, 2021. [7] 李美虹. 基于小波变换和神经网络的工业时序分析方法研究与应用 [D] . 沈阳: 中国科学院大学(中国科学院沈阳计算技术研究所), 2022. [8] 魏光涛, 王泽黎, 张晓晨, 等. 基于小波分解和LSTM的夜经济电力商户分类模型研究[J] . 科技与创新,2023(3):122 − 125. [9] 于博. 基于小波变换和卷积神经网络的时序分类方法研究[D] . 长春: 吉林大学, 2023. [10] 李梦, 黄章杰, 徐健晖. 基于深度学习和小波分析的LSTM-Wavelet模型股价预测[J] . 重庆工商大学学报(自然科学版),2023,40(2):99 − 105. [11] 任君, 王建华, 王传美, 等. 基于正则化 LSTM 模型的股票指数预测[J] . 计算机应用与软件,2018,35(4):44 − 48, 108. doi: 10.3969/j.issn.1000-386x.2018.04.008 [12] BALAJI E, BRINDHA D, VINODH KUMAR E L, et al. Automatic and non-invasive Parkinson’s dis-ease diagnosis and severity rating using LSTM net-work[J] . Applied Soft Computing,2021, 108: 107463. [13] 徐宝昌, 吕爽, 董秀娟, 等. 基于L2正则化LSTM 的非线性动态系统辨识[J] . 化工自动化及仪表,2021,48(1):1 − 7. [14] 苏东月. 基于Lasso方法与LSTM的股票价格预测[D] . 北京: 华北电力大学, 2022. [15] 宋旭东, 朱大杰, 杨杰, 等. 一种基于L2正则化迁移学习的变负载工况条件下故障诊断方 法[J] . 大连交通大学学报,2022,43(2):106 − 109, 114. [16] 黄培煜, 林雪, 谢镇涛, 等. 基于贝叶斯正则化LSTM模型的人均GDP预测效果: 以福建省为例[J] . 时代经贸,2023,20(6):140 − 144. doi: 10.3969/j.issn.1672-2949.2023.06.029 [17] 陈晓姨. 基于贝叶斯优化的CNN-LSTM股价预测模型[D] . 兰州: 兰州大学, 2023. [18] MORLET J, ARENS G, FORUTEAU E, et al. Wave propagation and sampling theory – part II: sampling theory and complex waves[J] . Geophysics,1982,47(2):222 − 236. doi: 10.1190/1.1441329 [19] HOCHREITER S, SCHMIDHUBER J. Long short-term memory[J] . Neural Computation,1997,9(8):1735 − 1780. doi: 10.1162/neco.1997.9.8.1735 [20] HOERL A E, KENNARD R W. Ridge regression: biased estimation for nonorthogonal problems[J] . Technometrics,1970,12(1):55 − 67. doi: 10.1080/00401706.1970.10488634 -

下载:

下载:

点击查看大图

点击查看大图

图(7) / 表(3)

计量

- 文章访问数: 981

- HTML全文浏览量: 831

- PDF下载量: 83

- 被引次数: 0